How to Prepare for the EU Carbon Border Adjustment Mechanism (CBAM) in 2026

By 1 January 2026, the EU’s carbon levy will transition from a simple reporting requirement to a mandatory financial obligation that could increase the landing cost of industrial imports by over 20 percent. Many UK businesses are already struggling with the technical complexity of calculating embedded emissions across non-EU factories. It’s understandable to feel concerned about the administrative weight of obtaining Authorised Declarant status and the sudden pressure on your margins. This article provides a comprehensive roadmap on how to prepare for the EU Carbon Border Adjustment Mechanism (CBAM) to ensure seamless customs compliance and maintain your competitive edge.

We’ll help you manage the shift from the transitional period to the definitive phase with precision. You’ll gain a clear compliance checklist, proven strategies to optimise your carbon costs, and an understanding of how your freight forwarder acts as a critical partner in managing this data. Let’s look at how you can build a smarter, more sustainable supply chain that’s ready for the 2026 deadline.

Key Takeaways

- Understand the critical transition from the transitional phase to the definitive phase on 1 January 2026, when carbon costs become a financial reality for imports.

- Identify the necessary steps to secure ‘Authorised CBAM Declarant’ status, ensuring your business maintains legal compliance and access to the EU market.

- Master the distinction between Scope 1 and Scope 2 emissions reporting to ensure accurate data collection and avoid the high costs of EU default values.

- Follow our expert 5-step roadmap on how to prepare for the EU Carbon Border Adjustment Mechanism (CBAM) through proactive scope audits and supplier engagement protocols.

- Discover how bespoke logistics solutions and AI-driven digital strategies can help your business optimise carbon costs and streamline complex customs documentation.

Understanding the EU CBAM Definitive Phase in 2026

The European Union’s Carbon Border Adjustment Mechanism (CBAM) represents a fundamental shift in global trade dynamics. It’s designed as a regulatory tool to prevent carbon leakage, which occurs when EU-based companies move carbon-intensive production to countries with less stringent climate policies. By placing a carbon price on imports, the EU ensures that the environmental costs of production are accounted for, regardless of where the goods originate. For UK exporters and global logistics partners, Understanding the EU CBAM is no longer optional; it’s a core requirement for maintaining market access and price competitiveness.

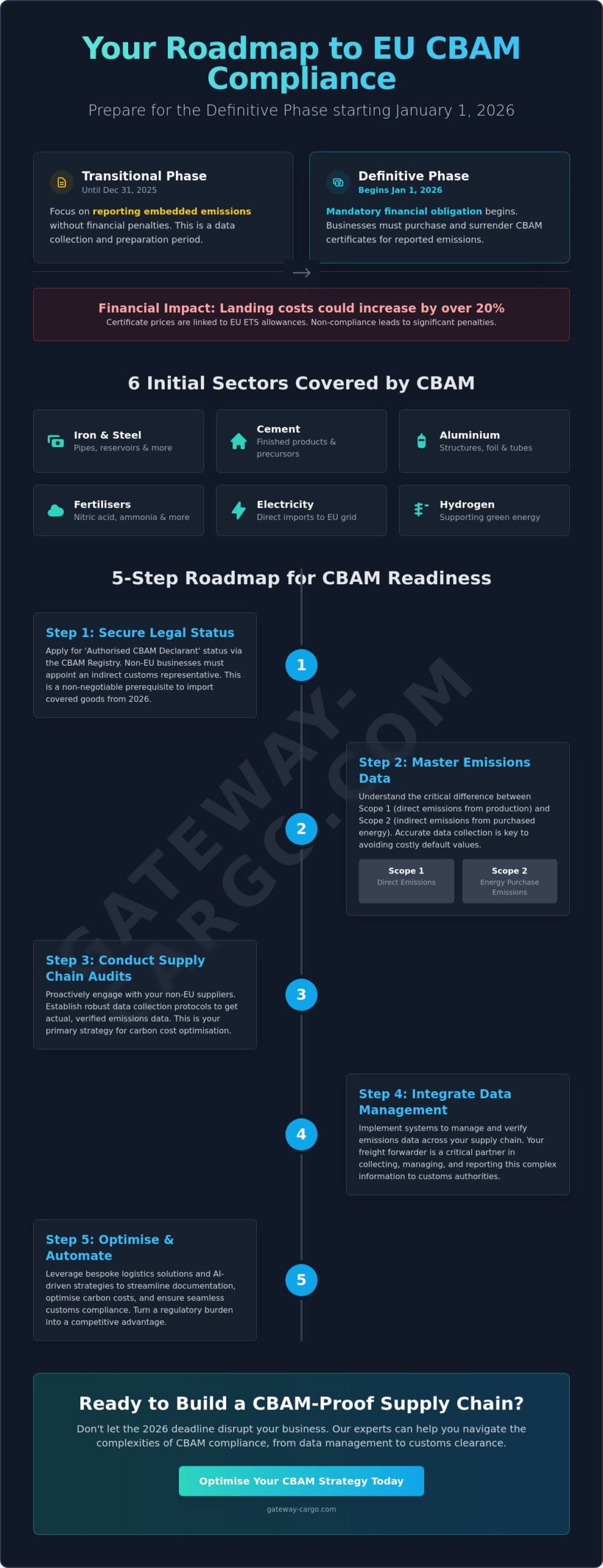

The Transitional Phase ends on December 31, 2025. During this initial period, businesses only needed to report emissions data without any financial exchange. However, on January 1, 2026, the Definitive Phase begins. This shift introduces actual financial obligations for six initial sectors:

- Cement: Includes finished products and precursors.

- Iron and Steel: Covers a wide range of downstream products like pipes and reservoirs.

- Aluminium: Includes structures, foil, and tubes.

- Fertilisers: Focuses on nitric acid, ammonia, and mixed fertilisers.

- Electricity: Direct imports into the EU grid.

- Hydrogen: Added to the scope to support the green energy transition.

The Financial Impact of Carbon Pricing

The core of the definitive phase is the mandatory purchase of CBAM certificates. These aren’t fixed fees; their price tracks the weekly average auction prices of EU ETS allowances. While these are often quoted in Euros, they directly impact the total £ cost of landed goods for UK firms. As the EU gradually phases out free carbon allowances for domestic manufacturers between 2026 and 2034, the cost of these certificates will likely increase to maintain a level playing field. Importers must surrender the required number of certificates by May 31, 2027, to cover the embedded emissions of goods brought into the EU during the 2026 calendar year. Relying on default emission values rather than actual verified data could lead to significantly higher certificate costs, making precise carbon accounting a financial necessity.

Why 2026 is the Critical Turning Point for Shippers

The transition from 2025 to 2026 marks the move from administrative compliance to direct financial liability. Knowing how to prepare for the EU Carbon Border Adjustment Mechanism (CBAM) now is vital to protect profit margins and ensure liquidity. In 2025, errors in reporting might lead to requests for clarification. In 2026, non-compliance results in significant financial penalties and potential cargo holds at the border. According to recent supply chain news today, regulatory volatility is a top risk for global logistics. Shippers who fail to secure authorised CBAM declarant status before the 2026 deadline will face immediate disruptions at EU ports of entry. This status is a prerequisite for importing the covered goods, meaning a lack of preparation could halt trade flows entirely.

Securing ‘Authorised CBAM Declarant’ Status and Compliance

From 1 January 2026, the transitional phase ends and the definitive CBAM regime begins. Only an “Authorised CBAM Declarant” can legally import covered goods such as steel, aluminium, cement, and fertilisers into the EU market. This status isn’t granted automatically; it requires a formal application process that UK businesses must initiate well in advance. Understanding this registration is a core part of how to prepare for the EU Carbon Border Adjustment Mechanism (CBAM) to avoid costly border delays or rejected shipments.

The application process is managed through the CBAM Registry, a centralised electronic platform. You’ll need to apply via the National Competent Authority (NCA) in the EU Member State where your business is established. For UK exporters without a physical presence in the EU, you’re required to appoint an indirect customs representative. This representative will apply for the authorised status on your behalf and carry the legal responsibility for compliance. The vetting process is rigorous. Authorities will examine your financial solvency and your customs compliance history over the previous 36 months. Detailed information on these protocols is available in the Official EU Guidance on CBAM.

Responsibilities of the Authorised Declarant

Authorised declarants take on significant administrative and financial burdens. Every year, you must submit a CBAM declaration through the registry. This report details the total quantity of goods imported during the previous calendar year and the total embedded emissions associated with those products. By 31 May of each year, declarants must surrender a number of CBAM certificates that correspond to the amount of embedded emissions declared.

Record-keeping is equally vital. You’re required to maintain detailed documentation of emissions data and certification for five years. The EU Commission or National Competent Authorities can request these records for audits at any time. If your data doesn’t meet the required standards, you could face penalties ranging from £10 to £50 per tonne of unreported emissions.

The Role of Customs Clearance in CBAM

CBAM data must be fully integrated into your standard customs clearance workflows to ensure a smooth flow of goods. It’s no longer just about the value or origin of the product; the carbon footprint is now a mandatory data point for entry.

Precise HS codes are the foundation of this process. These codes determine whether your product falls under the CBAM scope. A single digit error in an HS code can result in non-compliance or unnecessary certificate costs. Gateway Cargo provides the technical expertise to manage these filings, ensuring that your emissions data aligns perfectly with your customs declarations. Our specialists help you how to prepare for the EU Carbon Border Adjustment Mechanism (CBAM) by auditing your current shipping data for accuracy.

If you’re looking to streamline your EU trade routes ahead of the 2026 deadline, contact our customs specialists

Data Management: Navigating Embedded Emissions Reporting

Reliable data management is the bedrock of compliance for UK importers. To understand how to prepare for the EU Carbon Border Adjustment Mechanism (CBAM), you must first categorise emissions correctly. Scope 1 emissions include all direct greenhouse gases (GHGs) emitted during the manufacturing process, such as those from furnaces or chemical reactions. Scope 2 emissions refer to indirect GHGs from the generation of electricity, heating, or cooling consumed during production. Accurate reporting requires a granular view of both categories across your entire supply chain.

The EU allows two primary reporting methods. During the initial transitional period, firms could use “Default Values” published by the European Commission. These are industry averages that often overestimate carbon intensity. From 2026 onwards, the definitive phase imposes a strict 20% limit on using default values for complex goods. This shift means 80% of your reported data must be “Actual Emissions” derived from primary sources at the manufacturing site. Failing to secure this data will likely result in higher carbon costs, as default values are intentionally penalising to encourage transparency.

Verification is another critical hurdle. From 2026, all reported emissions data must be validated by an EU-accredited third-party verifier. This independent audit ensures that the carbon intensity figures you submit align with EU standards before you surrender CBAM certificates. Preparing Your Business for CBAM involves establishing these verification channels now to avoid bottlenecks when the regulation fully takes effect.

Collaborating with Non-EU Suppliers

UK businesses must act as specialists in their own supply chains by requesting carbon intensity data from international manufacturing partners. Implementing a “Digital Product Passport” or a similar data-sharing framework helps standardise the information received. When suppliers are unable to provide verified metrics, you face a data gap that can lead to compliance failures. It’s essential to incentivise transparency; consider including carbon reporting requirements in your procurement contracts to ensure long-term data security.

Calculating the Embedded Carbon Footprint

Embedded emissions are the total GHGs released during production including heat and electricity. To calculate this, use the following simplified formula: Total Emissions = (Direct Emissions + Indirect Emissions) / Total Production Volume (tonnes). While “simple goods” only require data from the final production process, “complex goods” require you to account for the carbon footprint of upstream precursors. Understanding how to prepare for the EU Carbon Border Adjustment Mechanism (CBAM) means mapping these precursors to ensure every tonne of imported product is fully accounted for.

A 5-Step Roadmap to Prepare Your Supply Chain for CBAM

Transitioning from the current reporting phase to the definitive 2026 regime requires a structured technical approach. Businesses must align their internal procurement and compliance frameworks with EU regulatory standards to avoid operational delays. Understanding how to prepare for the EU Carbon Border Adjustment Mechanism (CBAM) involves more than just administrative filing; it requires a deep dive into your carbon footprint and financial liabilities.

- Step 1: Conduct a Scope Audit. Review every imported product against the Annex I list of the CBAM Regulation. This includes iron, steel, aluminium, cement, electricity, fertilisers, and hydrogen. Use specific HS codes to ensure no goods are missed during the classification process.

- Step 2: Supplier Engagement. Establish communication protocols now. You’ll need actual emissions data from your manufacturers rather than relying on default values, which the EU will phase out by 2026.

- Step 3: Financial Forecasting. Estimate the annual cost of CBAM certificates. Use the EU Emissions Trading System (ETS) price as your benchmark. In early 2024, prices fluctuated between £50 and £80 per tonne of CO2.

- Step 4: Registry Enrolment. Apply for Authorised CBAM Declarant status. Only authorised entities can import CBAM goods into the EU once the definitive period begins.

- Step 5: Process Integration. Embed reporting into your freight forwarder and ERP systems. This ensures that emissions data flows automatically from the point of origin to your final declaration.

Auditing Your Product Portfolio

Precision in inventory categorisation is vital for compliance. Use the EU’s official CBAM sector list to audit your current stock. Many businesses overlook “hidden” CBAM goods, such as steel components within complex machinery or aluminium brackets in consumer electronics. Accurate freight transport documentation must reflect these materials to prevent customs hold-ups. If a product contains more than 2% CBAM-regulated material by weight, it may require a declaration.

Financial Planning for Carbon Costs

The financial impact of CBAM depends on the “Carbon Price Paid” in the country of origin. You can claim deductions for carbon taxes already settled at the manufacturing site, provided you have verified evidence. Budgeting for the quarterly certificate holding requirement is also essential. By the end of each quarter, your account must hold at least 50% of the certificates required for the year’s projected emissions. Developing a strategy for purchasing these certificates, whether through spot buys or forward planning, helps mitigate price volatility in the carbon market.

Optimise your compliance strategy with expert logistics support. Contact Gateway Cargo today to secure your supply chain for 2026.

Optimising Compliance with Gateway Cargo’s Bespoke Logistics Solutions

Gateway Cargo integrates carbon reporting into the core of end-to-end supply chain management. We don’t just move goods; we provide the data infrastructure necessary for the 2026 transition. Our AI-driven digital strategy monitors freight emissions in real-time, offering a level of precision that manual spreadsheets cannot match. This technology is vital for UK exporters who need to account for every tonne of CO2 embedded in their products. Understanding how to prepare for the EU Carbon Border Adjustment Mechanism (CBAM) requires a partner who can translate complex emissions data into actionable customs declarations. We bridge the gap between your non-EU suppliers and EU customs authorities, ensuring that data flows as smoothly as the physical cargo.

Smarter Logistics for a Greener Future

Choosing the right transit paths is a strategic decision that affects your bottom line. By optimising ocean freight routes, we help clients reduce total emissions on specific lanes through better vessel utilisation and port selection. Our logistics specialists use data-led insights to avoid congested hubs and utilise established green logistics corridors. We offer bespoke freight solutions tailored to high-compliance industries like steel and aluminium, where the margin for error in carbon reporting is zero. To stay ahead of evolving EU environmental regulations, our clients rely on our “Insights” section and regular whitepapers. These resources provide the regulatory intelligence needed to adjust supply chain strategies before new costs take effect.

Partnering for CBAM Success

The role of the Authorised Declarant carries significant legal and financial responsibility under the new regime. A specialist freight forwarder is essential for managing this burden, as we verify that supplier data meets the EU’s rigorous verification standards. We act as your technical intermediary, preventing costly delays or penalties at the border. Our commitment to sustainability isn’t just theoretical; it’s backed by tangible investments in EV vehicles for last-mile delivery and partnerships in low-carbon transport networks. We help you identify how to prepare for the EU Carbon Border Adjustment Mechanism (CBAM) by conducting thorough audits of your current logistics framework. This proactive approach identifies potential gaps in data collection before they become compliance liabilities.

- Customs Expertise: We manage the complexities of EU entry points to ensure seamless clearance.

- Data Integrity: Our digital tools provide a transparent audit trail for all embedded emissions.

- Sustainability Focused: We prioritise carriers and routes that align with your ESG targets.

Consult with our logistics specialists today for a comprehensive CBAM readiness audit. We’ll help you navigate the reporting requirements and implement the technical changes needed for 2026. Optimise your supply chain with Gateway Cargo today to secure your competitive advantage in the European market.

Secure Your Competitive Edge for the 2026 Definitive Phase

The shift to the CBAM definitive phase on 1 January 2026 marks a pivotal change for UK exporters. You’ll need to transition from reporting estimated values to providing verified data on actual embedded emissions for every shipment. Managing this level of granular detail requires a robust digital framework and a deep understanding of EU customs regulations. Securing your ‘Authorised CBAM Declarant’ status early is essential to maintain seamless access to the European market and avoid potential financial penalties.

Learning how to prepare for the EU Carbon Border Adjustment Mechanism (CBAM) involves more than just administrative adjustments. Gateway Cargo supports your transition through an AI-driven digital strategy that provides real-time visibility and a dedicated team of customs clearance experts. We’ve invested in proactive sustainability solutions, including EV vehicle fleets, to help reduce your carbon footprint at the source. Our specialists ensure your data management aligns with the latest 2026 requirements, protecting your operations from non-compliance risks.

Contact our logistics specialists for a CBAM readiness audit to safeguard your supply chain today. We’re ready to help you navigate these regulatory shifts with confidence.

Frequently Asked Questions

What is the current price of a CBAM certificate in 2026?

The price of a CBAM certificate in 2026 is linked directly to the weekly average auction price of EU ETS allowances. As of early 2024, EU ETS prices fluctuate between £51 and £68 per tonne of CO2. Importers must monitor the European Commission’s weekly price publications to budget for these costs accurately. Your total certificate expenditure depends on the specific carbon intensity of your imported goods at the time of entry.

Can I import steel or aluminium without being an Authorised CBAM Declarant?

You cannot import steel or aluminium into the EU after 1 January 2026 unless you hold the status of an Authorised CBAM Declarant. This regulation applies to all goods within the CBAM scope, including cement, fertilisers, and hydrogen. Importers must apply for this status through the CBAM Registry to ensure compliance and avoid border delays. Without this authorisation, EU customs authorities will block your shipments, causing significant disruptions to your supply chain.

How do I calculate embedded emissions if my supplier won’t provide data?

You must use default values published by the European Commission if your supplier fails to provide actual emissions data. These values represent the average emission intensity of the worst-performing producers within the EU for that specific product category. This often results in a higher tax liability than using actual data. To understand how to prepare for the EU Carbon Border Adjustment Mechanism (CBAM), you should prioritise establishing data-sharing agreements with your global suppliers immediately.

Are there exemptions for small shipments or specific countries?

Exemptions apply to consignments with a total value of less than €150, which is approximately £128, for goods falling within the CBAM scope. Certain countries that participate in the EU ETS or have a linked carbon market, such as Iceland, Norway, and Switzerland, are also exempt. Other territories, including the UK, currently require full reporting and certificate surrender. This is because the UK carbon market isn’t yet fully linked to the EU system for CBAM purposes.

What happens if I fail to surrender enough CBAM certificates by the deadline?

Failure to surrender sufficient certificates by the 31 May annual deadline results in a penalty of £85 per tonne of CO2 equivalent emitted. This fine is applied in addition to the requirement to purchase and surrender the missing certificates. Penalties are indexed to the European consumer price index, so the cost increases annually. Repeated non-compliance can lead to the revocation of your Authorised CBAM Declarant status and restricted access to the European market.

How does CBAM interact with existing EU customs duties and VAT?

CBAM operates as a separate environmental levy alongside existing EU customs duties and Value Added Tax. It’s not a customs duty, but it’s collected through a similar administrative framework. When calculating your total landed cost, you must factor in the CBAM certificate price as a distinct line item. Learning how to prepare for the EU Carbon Border Adjustment Mechanism (CBAM) involves integrating these carbon costs into your financial forecasting and VAT recovery processes for 2026.

Is the UK CBAM the same as the EU CBAM?

The UK CBAM is a separate regulation scheduled to take effect on 1 January 2027, one year after the EU’s definitive phase begins. While similar in purpose, the UK version includes different product categories like glass and ceramics which aren’t currently in the EU scope. UK businesses exporting to Europe must comply with EU rules in 2026. Those importing into Britain must prepare for the domestic scheme and its specific reporting requirements the following year.

Can my freight forwarder act as my indirect representative for CBAM?

Your freight forwarder can act as an indirect customs representative for CBAM if they agree to take on the legal obligations of a declarant. In this arrangement, the forwarder becomes responsible for reporting emissions and surrendering certificates on your behalf. Many logistics providers require specific indemnity agreements before accepting this role due to the financial risks. It’s a practical solution for UK businesses that don’t have a physical presence or an EORI number within the EU.